Buyer Information

What To Know As A Buyer

What you should expect from any real estate agent

Here’s What You Should Expect From Any Agent You Work With:

You should expect to be treated with respect, not like a number. You should feel like the agent’s only client, not like transaction #34. You should expect to have your best interests represented. The whole moving process should be as painless as possible. Your agent’s eye shouldn’t be on your wallet, but on serving you selflessly. Your agent should not think of you as a transaction that will be gone in a few months, but more like a friend and a client for life.

You should expect your agent to work as hard for you as he would if he were buying or selling his own house. You should expect the highest skills available. Your calls should be returned promptly, you should be kept up to date, and not feel like you were forgotten by your agent.

If any problems do arise, your agent should go overboard to fix them and document everything diligently so that you are protected. After the transaction, you should expect your agent to be a trusted advisor that you can consult anytime. You should feel like you were represented professionally, and that you came out the better for it.

Why We Have a Lot to Lose!

Our business is built on referrals. What this means to you is that we don’t spend a lot of time on prospecting activities to find new clients as other agents do. So you get all of our attention and energy. We feel that by providing you with the best real estate experience you ever had, you will naturally want your friends and associates to have the same benefit. When this happens, we can devote even more time to making our service the best available.

Since we don’t knock on doors or make cold telephone calls, we depend on referrals to grow our business. We HAVE TO give you excellent service. You MUST be happy, or there will be no referrals from you, and our business will suffer. So we don’t see you as just a transaction, here today and gone tomorrow. We’re not superstars, pushing people through some kind of assembly line, but we see ourselves as super servants. We treat your business with great respect, and want to be your REALTORs for life.

What is a short sale?

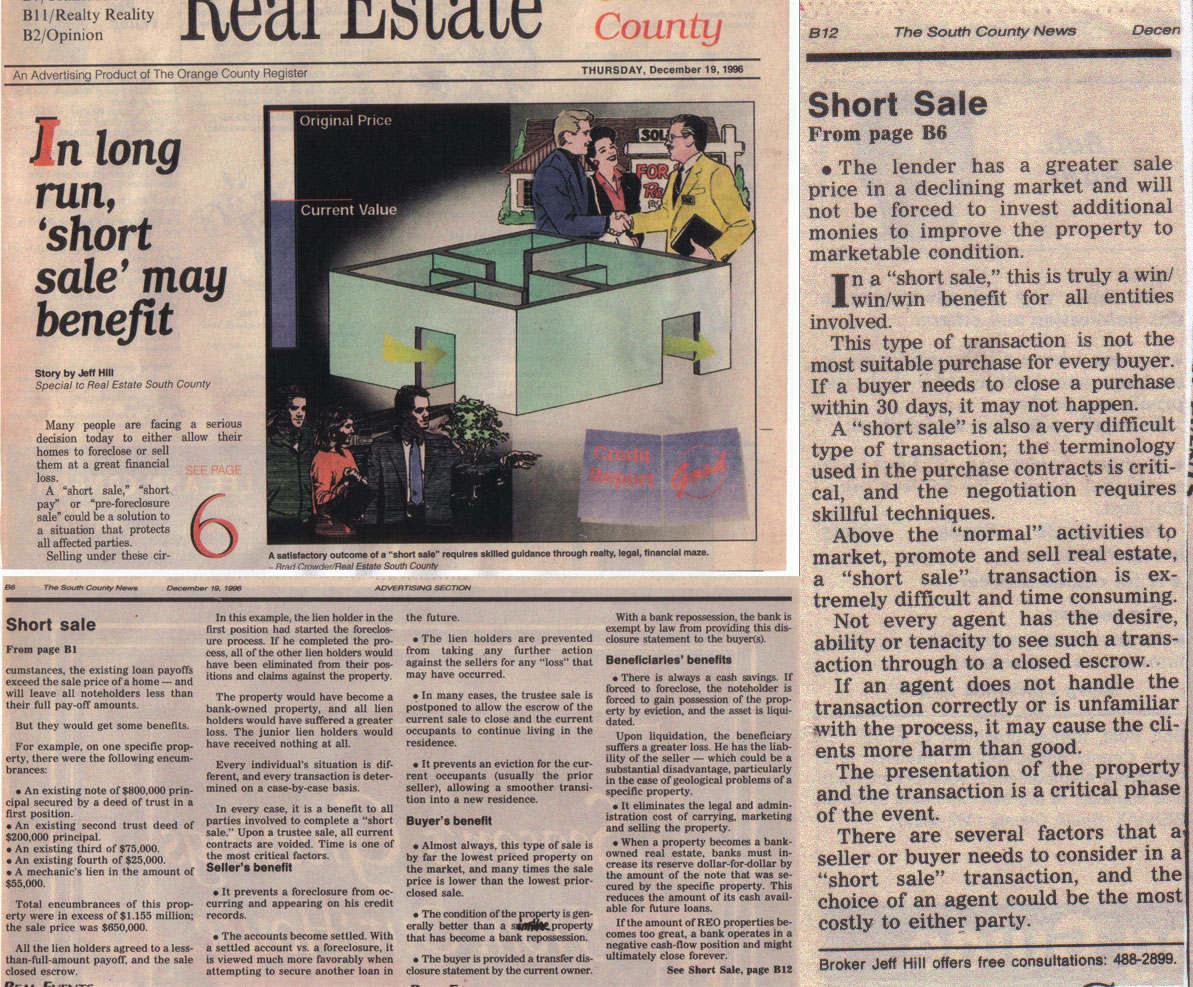

In some areas of the country, and from time to time, real estate values decline. In such situations it sometimes happens that owners need to move but the value of the mortgage is greater than the value of the property. The owner is said to be financially “upside down.”

In some areas of the country, and from time to time, real estate values decline. In such situations it sometimes happens that owners need to move but the value of the mortgage is greater than the value of the property. The owner is said to be financially “upside down.”

If the property is sold at a loss, the owner is still responsible for repaying the entire mortgage. But, sometimes owners do not have enough cash to re-pay the loan and so they try to work out a deal with the lender to pay less than is owed — a short sale.

The lender, of course, wants back every dime loaned to the borrower. That was the deal. And lenders point out, properly, that if the value of the property rose the borrower would not turn around and offer some of that profit to the mortgage company.

Lenders will sometimes allow a short sale if it is a better alternative than a foreclosure sale in a down market. However, before making such a decision, a lender will want to see how such a deal can be structured. Perhaps the borrower has other assets, or perhaps the short-fall can be made up with a note to the lender.

If the lender takes a loss, that loss may be reported to the IRS as income to the borrower — money not actually received by the borrower, but money that is taxable. There are exceptions to the discharged debt from being taxable income! Please Google Internal Revenue Code Section 108. In addition to Section 108 of the Internal Revenue Code, the Government passed H.R. 1876: Mortgage Cancellation Relief Act of 2007. See a tax professional for details before making any decisions.

In the event that a borrower faces a short sale situation, if you would like to keep your home, one approach is to have an attorney contact the lender on your behalf. It may be possible to work out a different monthly payment, an interest rate lowered to current levels, a long extension, etc.

Another alternative is to rent the property.

If the property is rented, it may then be possible to write off any losses. In contrast, with a primary principle place of residence property, it is not possible to write off losses at this time.

If you must move, a short sale is usually the best alternative for all parties involved. BE VERY CAREFUL OF THE AGENT YOU SELECT! The choice of listing agent will be the SINGLE MOST IMPORTANT decision if a short sale is completed, or you end up with a foreclosure on your record for the next SEVEN YEARS!

Every agent is an independent contractor, no matter the “company” or franchise of affiliation. How the listing agent handles the short sale listing, will mean the difference between a closed short sale transaction, and a foreclosure for the seller!

I have met many agents in my Real Estate career, most hate short sales, most do not really know what to do, and not a one has the ratio of closed short sales that I personally have closed. I have closed short sales with FIVE, and up to EIGHT liens of record! All lien holders of record MUST release their interest, or the sale will not close. My personal closing ratio of short sale listing is over 90%.

Real Estate is a practice, like law and medicine. Market conditions, availability of funds, qualifying criteria of borrowers, FHA, FANNIE MAE loan limits change, everything changes. What may have worked in the past, may not work today. Be sure the Real Estate Agent you hire is looking out for YOUR best interest, not THEIR income! If the agent only list properties, or has a “staff” of people that work under him/her, chances are very good YOU are not their priority, only their income is a priority!

There is no guarantee a short sale transaction will close. Every short sale is evaluated on a case-by-case basis. With the seasoned agent, that knows the route to a successful approval from each lender of record, you can have a successful sale and closed sale too.

Remember this; The value of an agent, is in their ability to negotiate.

Appraisals & Sales Price

When the property appraises for a lower value than the sales price, the lower appraised value is used to determine your loan amount. To complete the sale, you may have to increase the down payment to make up the difference between the appraised value and the purchase price.

The Appraisal Process

An appraisal is a written estimate of a property’s market valueMarket Value - The highest price a buyer will pay for a property and the lowest price the seller will accept in a typical market. completed by an appraiser. The value is based upon a market analysis of the prices of recent sales of similar properties in the area and the property’s physical condition. Usually, this requires an interior and exterior property inspection.

Why is an Appraisal Necessary?

Lenders use your appraisal to determine your loan amount. Your appraisal will be completed shortly after you request your mortgage.

Real Estate Glossary

Real Estate Glossary & Definitions

Property Definitions | Real Estate Terminology

Property Definitions

Single Family Residence

A structure that provides housing accommodations for one single family. ^

Condominiums

A condominium is a home in a shared building or development. The buyer gets title the space inside the unit, shares the common areas with other unit owners and pays a maintenance fee to the condominium association to pay for needed maintenance, repairs and improvements to the property. ^

Duplex

A structure that provides housing accommodations for two families by having separate entrances, kitchens, bedrooms, lanais, living rooms and bathrooms. A two-family dwelling. ^

Triplex

A structure that provides housing and accommodations for three families by having separate entrances, kitchens, bedrooms, lanais, living rooms and bathrooms. A three-family dwelling. ^

Fourplex

A structure that provides housing and accommodations for four families by having separate entrances, kitchens, bedrooms, lanais, living rooms and bathrooms. A four-family dwelling. ^

Multiple Family Dwellings

A Duplex, Triplex , Fourplex or more. Can also refer to an apartment or condominium complex. ^

Commercial Property

A classification of real estate which includes income producing property such as office buildings, gasoline stations, restaurants, shopping centers, hotels and motels, parking lots and stores, and other similar uses. ^

Industrial

An area zoned industrial and containing sites for many separate industries and developed and managed as a unit, usually with provisions for common services for the users. ^

Raw or Vacant Land

Unimproved land; land in its unused natural state prior to the construction of improvements such as streets, lighting, sewers, and the like. ^

Escrow

Money or other valuables given to a neutral third party with directions to deliver them to another party upon the fulfillment of a specific act or condition. ^

Title Insurance

Protection for lenders and homeowners against financial loss resulting from legal defects in or other claims against the property’s title. The cost of the policy is usually a function of the value of the property and is often borne by the purchaser and or seller. ^

Real Estate Terminology

Abstract (Of Title)

A summary of the public records relating to the title to a particular piece of land. An attorney or title insurance company reviews an abstract of title to determine whether there are any title defects which must be cleared before a buyer can purchase clear, marketable, and insurable title. ^

Acceleration

The right of the mortgagee (lender) to demand the immediate repayment of the mortgage loan balance upon the default of the mortgagor (borrower), or by using the right vested in the Due-on-Sale-Clause. ^

Acknowledgment

A formal declaration before an authorized official (usually a notary public) by a person who has executed a document, that he did in fact execute (sign) the document. ^

Addendum

Something added. A list or other items added to a document, letter, contract, escrow instructions, etc. ^

Agent

A person who acts or has the power to act for another. A real estate agent acts on behalf of the principal (the buyer or seller) and has a fiduciary responsibility towards the principal. Buyer’s Agent: a agent who represents the buyer and owes fiduciary duties to the buyer. Seller’s Agent: an agent who represents the seller and owes fiduciary duties to the seller. They are usually referred to as the listing agent who is authorized by a property owner to find a buyer or a tenant for the property. ^

Agreement of Sale

A written agreement of contract in which the seller agrees to sell and the buyer agrees to buy under specific terms and conditions. ^

Alienation Clause

A clause within a loan instrument calling for a debt in its entirety upon the transfer of ownership of the secured property. Also called a “due on sale” clause. ^

Amenities

Features that enhance and add to the value or desirability of real estate. Common amenities include swimming pools, professional landscaping, gourmet kitchen and so on. ^

Amortization

The reduction of a debt over time by making periodic payments, usually monthly, a portion of which is interest and a portion of which reduces the outstanding amount of the debt. The monthly mortgage payments remain the same over the life of the loan, even though the proportion of principal to interest changes over time. In the early part of the loan period the principal repayment is very small and interest repayment is very high. At the end of the loan that relationship is reversed. ^

Appraisal

An estimate of the value of property, made by a qualified professional called an “appraiser”. ^

Appraiser

Someone who practices appraisal. Appraisers’ work involves appraising, review (the process of critically studying a report prepared by another), or consulting (the process of providing information, analysis of real estate data, and recommendations on diversified problems in real estate, other than estimating value). ^

APR – Annual Percentage Rate

The actual interest rate taking into account the points and other prepaid fees expressed in annual percentage terms. Not to be confused with initial interest rate, a teaser rate lenders use to get you into a loan. ^

ARM – Adjustable Rate Mortgage

A loan that allows the interest rate to change periodically up or down. The interest rate on an ARM is determined by adding a margin or spread to a specified financial index. Financial indexes include; Treasury, Certificate of Deposit, Cost of Funds. The margin is the difference between the index rate and the ARM rate. Adjustment interval is how often the interest rate is adjusted. A loan that adjusts its interest rate after six months is called a six-month ARM. Rate caps limit how much your interest rate can move up or down. Periodic caps limit the change per adjustment period, and a lifetime cap governs the maximum amount the interest rate can increase or decrease over the life of the loan. ^

Assessment

A local tax levied against a property for a specific purpose, such as a sewer or street lights. ^

Assessor

One appointed to assess property for taxation. ^

Assignment

A transfer or making over to another the whole of any property, real or personal, or of any estate or right therein. To assign is to transfer. ^

Assumption

The agreement between the buyer and seller where the buyer takes over the payments on an existing mortgage from the seller. Assuming a loan can usually save the buyer money since this is an existing mortgage debt, unlike a new mortgage where closing costs and new, probably higher, interest rates will apply. ^

Balloon Mortgage

A mortgage for a fixed term shorter than necessary to fully repay the debt. As a result, the remaining amount of principal is due at the maturity of the loan. ^

Blanket Mortgage

A mortgage covering at least two pieces of real estate as security for the same mortgage. ^

Bond

An insurance agreement by which one party is insured against loss or default by a third party. In the construction business a performance bond ensures the interested party that the contractor will complete the project. ^

Breach

Violation of an obligation in a contract. ^

Bridge Loan

A loan, usually short term, that finances the portion of the purchase price not provided by the mortgage loan and the down payment. A bridge loan is commonly used when a purchaser has not sold his existing home before he closes on his purchase of a new home. The bridge loan is paid off when the old home is sold, out of the proceeds of that sale. ^

Broker

A real estate professional who has acquired a higher level of training and experience than a sales agent. A minimum number of classes must be taken along with passing a state exam to acquire a brokers license. Generally they are a legal representative or a proprietor of the office. Brokers usually charge a fee or receive a commission for their services. ^

Building Code

A set of stringent laws that control the construction of buildings, design, materials and other similar factors. ^

Building Line or Setback

Distances from the ends and/or sides of the lot beyond which construction may not extend. The building line may be established by a filed plat of subdivision, by restrictive covenants in deeds or leases, by building codes, or by zoning ordinances. ^

Buy-down

When the lender and or the home builder subsidized the mortgage by lowering the interest rate during the first years of the loan. While the payments are initially low, they will increase when the subsidy expires. ^

Buyers Market

A market condition which occurs in real estate where more homes are for sale than there are interested buyers. ^

Cash Flow

The amount of cash derived over a certain period of time from an income-producing property. The cash flow should be large enough to pay the expenses of the income producing property (mortgage payment, insurance, maintenance, utilities, etc.) ^

Capital Gain

Income that results from sale of a capital (tangible) asset. ^

Capitalization

An appraising term used in determining value by considering net operating income and a percentage of reasonable return on investment. ^

Certificate of Eligibility

The document given to qualified veterans which entitles them to VA guaranteed loans for homes, business, and mobile homes. Certificates of eligibility may be obtained by sending DD-214 (Separation Paper) to the local VA office with VA form 1880 (request for Certificate of Eligibility). ^

Chain Of Title

A history of conveyances and encumbrances affecting the title as far back as records are available. ^

Closing

The end of the transaction when the seller hands over the title to the buyer in exchange for payment. Also called settlement. ^

Closing Costs

Costs the buyer must pay at the time of the closing in addition to the down payment which may include points, title charges, credit report fee, document preparation fee, mortgage insurance premium, inspections, appraisals, prepayments for property taxes, deed recording fee, and homeowners insurance. Closing costs can vary considerably from one financial institution to another. ^

Cloud (On Title)

An outstanding claim or encumbrance which adversely affects the marketability of title. ^

Commission

Money paid to a real estate agent or broker by the seller as compensation for finding a buyer and completing the sale. Usually it is a percentage of the sale price: 4 to 7 percent on houses, 10 percent on land. ^

Condemnation

A declaration by governing powers that a structure is unfit for use. ^

Conditional Sales Contract

A contract for the sale of property where the buyer has possession and use, but the seller retains title until the conditions of the contract have been fulfilled. Also known as a land contract. ^

Condominium or Condo

A condominium is a home in a shared building or development. The buyer gets title the space inside the unit, shares the common areas with other unit owners and pays a maintenance fee to the condominium association to pay for needed maintenance, repairs and improvements to the property. ^

Construction Loan

A short term interim loan to pay for the construction of building or homes. These are usually designed to provide periodic disbursements to the builder as he progresses. ^

Contingency

A condition that must be met before a contract is binding. Contingencies include: the property must appraise for sales price or buyers approving of various inspections. ^

Contract Sale or Deed

A contract between purchaser and a seller of real estate to convey title after certain conditions have been met. It is a form of installment sale. ^

Conventional Loan

A fixed rate and fixed term loan that is made without government insurance. ^

Convertible Loan

Some ARM loans include a provision that allows it to convert to a fixed rate mortgage at specific times, usually from the end of the first through the fifth years. There is usually an additional fee, $300-$500, to convert it. ^

Conveyance

The transfer of the title to land from one to another. ^

Co-operative or Co-op

In a residential co-operative, the buyer purchases shares in the co-op corporation which is made up of the residents in the co-op property. The buyer owns the shares rather than owning real property. In exchange he has the right to lease and occupy a co-op unit. ^

Covenants

Agreements written into deeds and other instruments stating performance or non-performance of certain acts or noting certain uses or non-uses of property. ^

Credit Report / History

Lenders will investigate your credit record which is a history of your debts. They get a report from a credit reporting agency (TRW, Equifax, TransUnion) which shows if you pay you debts on time and with who you have current debts with. ^

Debt-to-income Ratio

The ratio, expressed as a percentage, which results when a borrower’s monthly payment obligation on long-term debts is divided by his or her gross monthly income. ^

Deed

A legal document by which property title is transferred from one owner to another. ^

Default

Failure to meet legal obligations in a contract, specifically, failure to make the monthly payments on a mortgage. ^

Depreciation

Decline in value of a house due to wear and tear, adverse changes in the neighborhood, or any other reason. ^

Devisee

A person who receives real estate from another by will. ^

Down Payment

The down payment is the percentage of the purchase price that the buyer must pay in cash and may not borrow from the lender. The down payment amount in addition to the mortgage equals the purchase price of a property. They can vary from 0% to over 50%. The less your down payment the better your credit has to be. Lower down payments generally result in higher interest rates. ^

Dual Agency

Representing both parties in a transaction. In virtually all states it is unethical and illegal for a broker to represent buyer and seller in a real estate transaction without written consent of both. ^

Due-on-Sale Clause

A provision in a mortgage or deed of trust that allows the lender to demand immediate payment of the balance of the mortgage if the mortgage holder sells the home. ^

Earnest Money

The deposit money given to the seller by the potential buyer as evidence of good faith in purchasing real estate. The broker places the money in an escrow or trust account until closing, when it becomes part of the down payment. ^

Easement Rights

A right- of- way granted to a person or company authorizing access to or over the owner’s land. An electric company obtaining a right- of- way across private property is a common example. ^

Economic Obsolescence

Loss of useful life and desirability of a property through economic forces, such as change in zoning, changes in traffic flow, etc., rather than deterioration. ^

Encroachment

An obstruction, building, or part of a building that intrudes beyond a legal boundary onto neighboring private or public land, or a building extending beyond the building line. ^

Encumbrance

A legal right or interest in land that affects a good or clear title, and diminishes the land’s value. ^

Equal Credit Opportunity Act (ECOA)

Is a federal law that requires lenders and other creditors to make credit equally available without discrimination based on race, color, religion, national origin, age, sex, marital status or receipt of income from public assistance programs. ^

Equity

The value of the property less the amount of unpaid mortgages and any outstanding liens. ^

Escalation Clause

A clause in a lease providing for an increased rent at a future time due to increased costs to lessor, as in cost of living index, tax increases, etc. ^

Escheat

The reverting of property to the state in the absence of heirs. ^

Escrow

Money or other valuables given to a neutral third party with directions to deliver them to another party upon the fulfillment of a specific act or condition. ^

Escrow Instructions

This discloses when the escrow should be closing and when possession should take place, proration of property taxes, transfer taxes, release of funds and the basics of satisfying the escrow demands. ^

Estate

The ownership interest of a person in real property. Is also used to refer to a deceased person’s property. ^

Exclusive Agency Listing

A written agreement giving the broker the right to market an owner’s property for a certain period of time, but also allowing the owner to sell the property during that period without paying a commission. ^

Exclusive Right-to-Sell

A written agreement between the agent and the owner whereby the owner promises to pay a fee or commission to the broker if his property is sold during the listing period, regardless of whether the broker is responsible for the sale. ^

Fair Market Value

That price a property will bring given that both buyer and seller are fully aware of market conditions and comparable properties. ^

Fannie Mae – FNMA

Nickname for the Federal National Mortgage Association. FNMA is a public corporation originally established by the federal government. Fannie Mae purchases mortgage loans from lenders and results in a major source of funds for mortgage companies. ^

Fee Simple

Ownership of title to property without any limitation, which can be sold, left at will, or inherited. ^

FHA – Federal Housing Administration

Part of the US Department of Housing and Urban Development (HUD). It was established in 1934 to encourage improvement in housing standards and communities. The FHA insures mortgage loans. ^

FHA Mortgage

A mortgage loan insured by the Federal Housing Administration. ^

FHA Mortgage Insurance

Requires a fee (up to 2.25% of the loan amount) paid at closing to insure the loan with FHA. In addition, FHA mortgage insurance requires an annual fee of up to 0.5% of the current loan amount, paid in monthly installments. The lower the down payment, the more years the fee must be paid. ^

Foreclosure

A legal process by which the lender or the seller forces a sale of a mortgaged property because the borrower has not met the terms of the mortgage. Also known as a repossession of property. ^

Freddie Mac – FHLMC

Nickname for Federal Home Loan Mortgage Corporation. It is a quasi-governmental agency that purchases conventional mortgages from insured depository institutions and HUD- approved mortgage bankers. ^

Functional Obsolescence

Loss in value due to out-of-date or poorly designed equipment while newer equipment and structures have been invented since it’s construction. ^

Ginnie Mae – GNMA

Government National Mortgage Association ^

Graduated Payment Mortgage – GPM

A type of flexible-payment mortgage where the payments increase for a specified period of time and then level off. This type of mortgage has negative amortization built into it. ^

Grantee

That party in the deed who is the buyer or recipient. ^

Grantor

That party in the deed who is the seller or giver. ^

Home or Property Inspection

A detailed inspection of the physical structure, the plumbing, electrical and heating systems and the overall condition of the home. Typically the cost is $150-$300 and the results are detailed in a multiple page report. ^

Homeowners Insurance

Insurance that protects the homeowners from Casualty losses or damage to the home or personal property and from liability damages to other people or property. Homeowners insurance is required by the lender and may be included in the monthly mortgage payment. ^

Home Owners Association

An association of homeowners within a community formed to improve and maintain the quality of the community. An association formed by the developer of condominiums or planned developments. ^

Housing Expense-to-Income Ratio

The ratio, expressed as a percentage, which results when a borrower’s housing expenses are divided by his or her gross monthly income. ^

HUD – The US Department of Housing and Urban Development

Department of Housing and Urban Development, a government agency created to make the American Dream of home ownership a real possibility for everyone. HUD has many programs involving homeownership assistance for low and moderate income families, community planning and development, fair housing and equal opportunity, and home improvement loans. The Housing and Urban Development home page is a rich resource of information. ^

HUD Home

When a purchaser fails to meet her/his obligation of a HUD insured loan and, the lender completes a foreclosure, ownership is then turned over to HUD. Only HUD approved brokers may sell HUD homes. ^

Impound

That portion of a borrower’s monthly payments held by the lender or servicer to pay for taxes, hazard insurance, mortgage insurance, lease payments, and other items as they become due. Also known as reserves. ^

Index

A published interest rate against which lenders measure the difference between the current interest rate on an adjustable rate mortgage and that earned by other investments (such as one-three and five-year U.S. Treasury security yields, the monthly average interest rate on loans closed by savings and loan institutions, and the monthly average costs-of-funds incurred by savings and loans), which is then used to adjust the interest rate on an adjustable mortgage up or down. ^

Initial Interest Rate

The initial rate quoted usually is a lower introductory rate, sometimes called a teaser or discount rate. This lower rate lasts only until the first adjustment, after which you will be charged the fully indexed rate. ^

Interest

A charge paid for borrowing money. ^

Joint Tenancy

Joint ownership by two or more persons with right of survivorship. Upon the death of a joint tenant, his interest does not go to his heirs, but to the remaining joint tenants. ^

Jumbo Loan

A loan which is larger than the limits set by the FNMA and FHLMC (more than $207,000 as of 1/1/96). Because jumbo loans cannot be funded by these two agencies, they usually carry a higher interest rate. ^

Lease

A contract between the owner of real property, called the lessor, and another person referred to as the lessee, covering all conditions by which the lessee may occupy and use the property. ^

Lease With Option To Purchase

A lease where the lessee has the option to purchase the leased property. The terms of the purchase option must be set forth in the lease. ^

Legal Description

The geographical identification of a parcel of land. ^

Lien

A hold or claim on the property of another to satisfy an unpaid debt or obligation. ^

Life Time Cap

Life time cap governs the maximum amount the interest rate increase or decrease over the life of the loan. ^

Listing Contract

An agreement between a homeowner and a licensed real estate broker that authorizes the broker to market the property for sale during a given time period. ^

Loan Origination Fee

A fee charged by the lender for evaluating, preparing and submitting a proposed mortgage loan. ^

Loan-to-Value Ratio

The ratio of a mortgage loan principal to the property’s appraised value or its sales price, whichever is lower. Loan-to-value ratios vary depending upon the individual lender’s policy. ^

Lock-in Rate

A commitment made by a lender to make a mortgage loan at a specified rate, pending loan approval, on or prior to a specified date. ^

Market Value

The highest price a buyer will pay for a property and the lowest price the seller will accept in a typical market. ^

Margin

The amount a lender adds to the index on an adjustable rate mortgage to establish the adjusted interest rate. ^

Mechanic’s Lien

A lien created by statute on a specific property for labor or materials contributed to an improvement on that property. ^

Mortgage

A lien on real estate given by the buyer to secure money borrowed to purchase the real estate. ^

Mortgage Broker

An individual or company that obtains mortgages for others by finding lending institutions, insurance companies or private sources to lend the money. The mortgage broker may also handle collections and disbursements. ^

Mortgage Insurance

A policy that provides protection for the lender in case of default and or which guarantees repayment of the loan if the borrower becomes disabled or dies. ^

Mortgage Insurance Premium – MIP

Insurance from FHA to the lender against incurring a loss on account of the borrower’s default. ^

Multiple Listing

A listing taken by a member of an organization of brokers, whereby all members have an opportunity to find a buyer. ^

NAR – National Association of Realtors

The largest trade association in the country serving over 700,000 Realtors. The purpose of the association is to enhance the ability and opportunity of its members to conduct business successfully and ethically and to promote the preservation of the right to own, transfer and use real property. ^

Negative Amortization

Occurs when your monthly payments are not large enough to pay all the interest due on the loan. This unpaid interest is added to the unpaid balance of the loan. The danger of negative amortization is that the home buyer ends up owing more than the original amount of the loan. ^

New Home

Accommodations having not yet been occupied. Usually purchased directly from the builder or developer. ^

Non Assumption Clause

A statement in a mortgage contract forbidding the assumption of the mortgage without the prior approval of the lender. ^

Notary Public

One who is authorized by federal or local government to attest authentic signatures and administer oaths. ^

Note

A written instrument acknowledging a debt and promising payment. ^

Offer

A proposal to purchase real estate at a particular price, subject to other specified terms and conditions. Acceptance of the offer by the seller creates a purchase contract. A counteroffer is a different offer made in response to the initial offer. ^

Origination Fee

Application fee(s) for processing a proposed mortgage. ^

Option

A right given, for consideration, to purchase or lease property upon stipulated terms within a specific period of time. ^

Periodic Caps

Periodic caps limit the change per adjustment period of a loan. ^

PITI Payment

A loan payment that combines Principal, Interest, Taxes and Insurance. ^

Plat

A map or chart of a lot, subdivision or community drawn by a surveyor showing boundary lines, buildings, improvements on the land, and easements. ^

PMI – Private Mortgage Insurance

Insurance issued to a lender to protect it against loss on a defaulted mortgage loan. Its use is usually limited to loans with high loan-to-value ratios, generally in excess of 80%. The borrower pays the premiums. ^

Point

An amount equal to one percent of the loan amount paid to a lender for making the loan. A lender may charge the borrower several points in order to provide the loan. ^

Power of Attorney

A legal document authorizing one person to act on behalf of another. ^

Prepayment

A privilege in a mortgage permitting the borrower to make payments in advance of their due date. ^

Prepayment Penalty

Money charged for an early repayment of debt. Prepayment penalties are allowed in some form, but are not necessarily imposed in many states. ^

Primary Mortgage Market

Lenders making mortgage loans directly to borrowers such as savings and loan associations, commercial banks, and mortgage companies. These lenders sometimes sell their mortgages into the secondary market such as FNMA or GNMA. ^

Pre-qualification

Getting pre-qualified for a loan is a free process and normally takes between 15 minutes to an hour on the phone. The lender will ask you some basic questions about your household income, time on the job, credit history, down payment and personal savings. You should get pre-qualified before looking for properties so you and your real estate agent know in what price range to start looking. ^

Principal

One of the parties to a transaction. For example, the buyer and seller are principals in the purchase of real property. Also the amount of debt, not counting interest, left on a loan. ^

Purchase Agreement

An agreement between buyer and seller denoting price and terms of the sale. ^

Rate Caps

Rate caps limit how much the interest rate can move up or down. ^

Real Estate Agent

A licensed person who works under the direction of a broker selling and renting real estate. ^

Real Estate Broker

A middle man or agent who buys and sells real estate for a company, firm, or individual on a commission basis. The broker does not have title to the property, but generally represents the owner. ^

Realtor

A Realtor is a real estate professional who is a member of the National Association of Realtors and subscribes to its strict Code of Ethics. This professional is committed to protecting and promoting private ownership of real property, establishing and maintaining high professional standards of practice, and creating unity in the National Association of Realtors organization and respect for the real estate profession. ^

Recision

The cancellation of a contract. With respect to mortgage refinancing, the law that gives the homeowner three days to cancel a contract in some cases once it is signed if the transaction uses equity in the home as security. ^

Refinance

Obtaining a new mortgage loan on a property already owned. Often to replace existing loans on the property. ^

R.E.O.

Real estate owned by a bank. A lending institution will acquire ownership of a specific property usually through a foreclosure process. ^

Repossessed

Same as R.E.O. ^

RESPA

Short for the Real Estate Settlement Procedures Act. RESPA is a federal law that allows consumers to review information on known or estimated settlement costs once after application and once prior to or at a settlement. The law requires lenders to furnish the information after application only. ^

Restrictive Covenants

Private restrictions limiting the use of real property. Restrictive covenants are created by deed and may “run with the land,” binding all subsequent purchasers of the land, or may be “personal” and binding only between the original seller and buyer. ^

Reverse Annuity Mortgage – RAM

A form of mortgage in which the lender makes periodic payments to the borrower using the borrower’s equity in the home as Satisfaction of Mortgage: the document issued by the mortgagee when the mortgage loan is paid in full. ^

Second Mortgage

A mortgage made subsequent to another mortgage and subordinate to the first one. ^

Secondary Mortgage Market

The place where primary mortgage lenders sell the mortgages they make to obtain more funds to originate more new loans. It provides liquidity for the lenders. ^

Seller’s Market

More buyers than sellers. ^

Shared Appreciation Mortgage – SAM

A mortgage in which a borrower receives a below-market interest rate in return for which the lender or investor, receives a portion of the future appreciation in the value of the property. May also apply to mortgage where the borrowers share the monthly principal and interest payments with another party in exchange for part of the appreciation. ^

Special Assessments

A special tax imposed on property, individual lots or all property in the immediate area, for road construction, sidewalks, sewers, street lights, etc. ^

Survey

A map or plat made by a licensed surveyor showing the results of measuring the land with its elevations, improvements, boundaries, and its relationship to surrounding tracts of land. ^

Title

Ownership of real property. Title is transferred from one party to another through a document called a deed. ^

Title Insurance

Protection for lenders and homeowners against financial loss resulting from legal defects in or other claims against the property’s title. The cost of the policy is usually a function of the value of the property and is often borne by the purchaser and or seller. ^

Title Search

An examination of municipal records to determine the legal ownership of property. Usually is performed by a title company. ^

Townhouse or Townhome

Used to describe an architectural style. A condominium with no one living above or below. ^

Trust

A property interest held by one person for the benefit of another. ^

Trustee

A party who is given legal responsibility to hold property in the best interest of or “for the benefit of” another. ^

Truth-In-Lending

A federal law requiring disclosure of the APR-Annual Percentage Rate to home buyers shortly after they apply for the loan. Also known as Regulation Z. ^

Underwriting

The decision whether to make a loan to a potential home buyer based on credit, employment, assets, and other factors and the matching of this risk to an appropriate rate and term or loan amount. ^

VA or US Department of Veterans Affairs

A federal agency designed and operated to help veterans enter the housing market. The VA assists veterans in terms of low or no down payment, mortgage qualifications assistance and low interest rates. ^

VA Home

When a purchaser fails to meet her/his obligation of a VA insured loan and, the lender completes a foreclosure, ownership is then turned over to VA. ^

VA Loan

A mortgage loan guaranteed by the US Department of Veterans Affairs against loss to the lender and made through a private lender. ^

Variable Interest Rate

A fluctuating interest rate which can go up or down depending on the going market rate. ^

Waive

To relinquish, or abandon. To forego a right to enforce or require anything. ^

Wraparound Mortgage

Results when an existing assumable loan is combined with a new loan, resulting in an interest rate somewhere between the old rate and the current market rate. The payments are made to a second lender or the previous homeowner, who then forwards the payments to the first lender after taking the additional amount off the top. ^

Zoning Ordinances

The acts of an authorized local government establishing building codes, and setting forth regulations for property land usage. ^

What EVERY buyer and seller should know!

By Jeffrey A. Hill, Real Estate Broker

Every time I speak with a seller or buyer, the following explanations prove fruitful:

Every time I speak with a seller or buyer, the following explanations prove fruitful:

Every agent is an independent contractor – No matter which company they work for, each agent is an independent contractor, and is self employed.

A seller may think they are hiring a company when they list a property with an agent who works for a franchise type of company. The Company is not going to do a thing for the client, only the agent will complete or not complete any activities associated with marketing a property. Use of a franchised name implies a company is there to represent you, and in fact, it is not.

Brokerage fees are customarily paid for by a seller. Buyers never pay brokerage fees, or do they? If a seller has no sale, are there any brokerage fees due to be paid? Buyers always pay brokerage fees, indirectly, in the form of a higher sales price. Although the fees do come directly from the seller’s side of a transaction, without a buyer there are no fees due. A buyer is the only one who ever pays the brokerage fees involved, indirectly in the form of a higher sales price.

Discount brokerage firms or FSBO. (For Sale by Owner)

A FSBO wants to “save” the brokerage fees. Who is saving them? Not the buyer if they pay the same price as a listing across the street that is listed by an agent. If a buyer wants to buy, are they going to look at other properties, or just one FSBO? An educated buyer will look at all available properties, including any FSBO’s or discount brokerage firms listings, and will make a decision based on the available properties, and what has sold within the last 3-6 months. 99% of all sales of homes are completed with the involvement of financing. A financing contingency is subject to an appraisal. The appraiser is limited to CLOSED sales that have occurred within the last 3-6 months. An appraiser will use a minimum of 3 similar properties within a one mile radius, make adjustments up or down for condition, location, square footage and any other amenity a comparable property features verses the subject property. To a degree, a seller is always limited to the last closed sales, with minor increases for market conditions (supply & demand). Example, if 3 exact model matches all sold for $500,000.00 within the last 3 months, with only slight variations, all with agents involved, the property in question (exact model) would be appraised at $500,000.00 If a FSBO wants $500,000.00 for their property, the chances are very high you can find a BETTER VALUE in a property that is listed with an agent down the street or within the same neighborhood! The FSBO’s property is worth $500,000.00 MINUS brokerage fees. If the FSBO agrees to sell to a buyer for $470,000.00, then the BUYER saves the brokerage fees.

A FSBO wants to “save” the brokerage fees. Who is saving them? Not the buyer if they pay the same price as a listing across the street that is listed by an agent. If a buyer wants to buy, are they going to look at other properties, or just one FSBO? An educated buyer will look at all available properties, including any FSBO’s or discount brokerage firms listings, and will make a decision based on the available properties, and what has sold within the last 3-6 months. 99% of all sales of homes are completed with the involvement of financing. A financing contingency is subject to an appraisal. The appraiser is limited to CLOSED sales that have occurred within the last 3-6 months. An appraiser will use a minimum of 3 similar properties within a one mile radius, make adjustments up or down for condition, location, square footage and any other amenity a comparable property features verses the subject property. To a degree, a seller is always limited to the last closed sales, with minor increases for market conditions (supply & demand). Example, if 3 exact model matches all sold for $500,000.00 within the last 3 months, with only slight variations, all with agents involved, the property in question (exact model) would be appraised at $500,000.00 If a FSBO wants $500,000.00 for their property, the chances are very high you can find a BETTER VALUE in a property that is listed with an agent down the street or within the same neighborhood! The FSBO’s property is worth $500,000.00 MINUS brokerage fees. If the FSBO agrees to sell to a buyer for $470,000.00, then the BUYER saves the brokerage fees.

If a seller fails to provide the required documentation to a buyer, and closes the transaction, the buyer may sue the seller in court. It is possible the seller could be liable for up to the sales price, and the buyer can possibly get a judgment against the seller for failing to disclose, or many other reasons. The court may require the seller to refund the buyer their money, and possibly impose punitive damages against the seller. Is it worth it? A question only you can determine!

Discount brokerage firms are like FSBO’s.

The way a buyer looks at the sale would be the same way a buyer looks at a FSBO. For a seller who considers a so called discount brokerage firm, that seller is getting just that, a discount agent. If an agent has initially agreed to work for less then the customary fees that other agents usually work for, HOW can a seller expect that agent to be skilled in negotiating the highest price for that seller? If the agent has began the transaction by first negotiating their own fees, you (buyer or seller) would have unrealistic expectations to think an agent who works for less, (less then is customary in the industry) and get the same results as an agent who refuses to begin the negotiating in a transaction with his or her fees. Common sense should tell you this. The agent will not have the ability to negotiate the highest price for the seller and a seller should not expect that from a discount agent or that seller or buyer has unrealistic expectations, just like a FSBO.

A buyer will make offers based on the fees that are being ‘saved’, and effectively no savings will occur.

Brokerage fees are not fixed by law, and will never be fixed. Although a usual and customary fee is charged for each side of a transaction. An agent who represents a seller is referred to as a listing agent. An agent who represents a buyer is referred to as a selling agent. In theory, the listing agent is attempting to obtain the highest price for the seller, and is first and foremost obligated to the seller to obtain this goal. The selling agent is obligated to the buyer to obtain the lowest price for the buyer. An obvious conflict of interest exist in theory, although it is legal for a buyer to be represented by the listing agent, the conflict of interest is apparent to most buyers. Every seller has their own personal situation and circumstances. For a buyer to get a “good deal” on a property, all the buyer needs is to have a very motivated seller! A discount brokerage firm will provide just that, a discount in service and ability, not the sales price, and not a motivated seller!

The value of an agent is in their ability to negotiate.

The value of an agent is in their ability to negotiate.

I say this twice because it is the ONLY value of an agent.

With the invention of the internet, anyone can pull up a list.

A taxicab service can drive you around.

The only value of a Real Estate Agent is in their ability to negotiate the highest price for a seller, or the lowest price for a buyer.

How do I find a good agent?

Referral from a friend or relative! A good agent is usually very busy.

I personally work mostly by referral. I have been successful for a great deal of sellers AND buyers, and have a constant, steady stream of referrals from hundreds of satisfied clients. This is one sure way to tell the agent has refined skills in negotiating and communicating. The length of time agent is licensed is no indication of their ability. A good agent should be able to produce several, if not a hundred satisfied customers. I personally can produce hundreds!

Most agents think only of how much is in the sale for them!

If you have looked for an agent at all, the chances are very high you have met one or more. When an agent has only their pay check in mind, it does cloud their ability to do the best job for a client (buyer, seller OR borrower).

Statistically over 80% of agents that obtain a Real Estate license are in the business for 2 years or less.

Statistically about 94% of agents make very little or no income from the real estate industry.

There are agents who have been BROKERS for over 20 years and still make very little, and continue to provide a disservice to the general public. I believe it is because they first think of themselves and not the client.

The very first and most important issue at hand is the client’s needs. If an agent thinks of what the client needs 1st, that agent will get paid as a by-product of servicing the client. This is a well known fact in the Real Estate industry, as well as many other industries.

Some things to remember:

You get what you pay for, sometimes less.

You can lead a horse to water, you cannot make them drink. (Unrealistic expectations)

Lenders

The saying in the industry is, “Lenders lie like rugs! All the time!” Why did lenders get that reputation? From lying all the time! It is a deserved reputation, and you may have an experience yourself.

The saying in the industry is, “Lenders lie like rugs! All the time!” Why did lenders get that reputation? From lying all the time! It is a deserved reputation, and you may have an experience yourself.

Here are some lies in advertising for you to call the lender on:

- No Cost, No Fees!

- No Points, No Closing cost, only $99.00 flat fee!

- You want a $200,000.00 loan; you’ll get a $200,000.00 no extra cost!

- A $200,000.00 loan or a $600,000.00 loan, you get the same rate!

- Good credit, bad credit, no credit, no problem.

- Good credit or bad credit, you’ll get the same low rate!

- Why should we charge you points or fees, were making enough over the life of the loan!

- We’ll come out and mow your lawn and wash your windows!

How can a lender advertise such blatant non-truths? The exact wording was structured to miss-lead the client to call the number advertised. Each individual borrower’s circumstance and qualifying abilities are different. If a borrower has a perfect credit history, is anyone going to provide a loan at the same rate as a borrower with poor credit? Common sense should answer those questions for you. W.C. Fields said it best; “There’s a sucker born every minute”. With the rate children have been born since he made that statement, it’s safe to say every 30 seconds or less!

Here is how the Mortgage industry works:

It is now like a giant machine, producing billions of dollars for borrowers and lenders alike.

A borrower walks into a retail branch of their local bank. That borrower is promised a loan amount, interest rate at a specific cost or no cost. (Retail rate)

The same borrower applies with me as a mortgage broker or company. I submit the borrower to the EXACT SAME BANK. The bank will extend a WHOLESALE RATE to me as a broker, on the average 2% of the loan amount in the form of a rebate. The exact same loan is obtained from the exact same lender for the exact same price, only I earned 2% of the loan amount. To save the borrower money, I can give a refund to the borrower, and the borrower ends up with a loan BELOW retail cost! This is the only way a borrower can get a loan below retail rates.

The difference between wholesale and retail is usually 2% of the loan amount!

Most times, the lender or bank will say to the borrower that they do not fit the loan program that was originally offered, and they have another one that the borrower will qualify for. If a bank tells you the programs they have for you are unavailable, and they want to get financing from another source, the bank then acts in the role of a broker.

A broker can search thousands of sources, including all the major lending institutions, and provide a borrower with more options then a single institution. The reputation I mentioned above was earned! The mortgage broker will want to charge origination fees, plus get a rebate, administration fees, processing fees, and any other fees they can get away with. If a mortgage broker can make 4% to 5% they are happy! They do not care to provide a client with the lowest rate at the lowest cost. Most Americans call this capitalism. If you go to your job, and the employer pays you double your paycheck for the same job, would you complain? What if your employer told you that they found someone that would work for 25% less then they are paying you? That you had a choice to accept less or they would hire the other employee? Would you accept less for the same job? This is exactly what happens every day across America in the Mortgage industry.

There are thousands of different loan programs available depending on your (the borrower) qualifying ability. All 3 of the major credit repositories have web sites that explain the “prime” borrower referenced in so many advertisements.

The “Prime” Borrower

The “prime” borrower will qualify by getting a loan for a home with a 20% down payment. This is so the borrower has enough of an investment at risk, in the event of a default of payments to the lender; the lender can foreclose on the borrower and liquidate the property without a financial loss to the lending institution. The “prime” borrower will have ‘AAA’ credit rating, owner occupy the subject property, and have a maximum loan amount below conforming loan limits. Conforming loan limits as of December 2004 were $359,650.00. This limit changes as the inflation increases within the United States. In 1989 the conforming loan limit was $203,150.00

Above this limit, the loan becomes what is known as a jumbo loan. Today (June 2005) the jumbo loan limit goes up to $750,000.00 in California, (some lenders will only go to $650,000.00) and over that amount, the loan is called a Super Jumbo Loan.

The higher the loan amount, the higher the interest rate.

The lower the credit score, the greater the risk for the lender, the higher the rate they will charge.

There are loans now available for a borrower to purchase up to $1.5 million purchase price or refinance with ZERO down payment, (100% of the value of the property).

The “prime” borrower will have the ability to document their income for the last two years, (tax returns) and have a DTI (debt to income) of 32% of the borrower’s NET income. To determine your DTI first average your monthly NET (after income tax) income. Then multiply that average monthly NET by 32% or 0.32. From that number, subtract any current debt obligations (monthly payments for a car, credit cards, or any other monthly debt you make payments on that has a 10 month or longer time to pay off) and the amount of monthly income is equal to the amount of monthly payment you can make for the TOTAL cost of a property in question. Total monthly payment includes Principle, interest, taxes (real property tax), insurance, association dues (if applicable) mello roos and any other cost associated with the specific property you are interested in. That is the “PRIME” borrower. 32% of your NET income minus current debt obligation equals total PITIA & MR. PLUS maximum loan to value (LTV) of 80%, owner occupied with a maximum loan amount within conforming loan limits.

In Southern California you would need to make a million dollars a year to buy a condo in some areas.

This is where the “sub-prime” market takes place.

All that term means is any borrower that is NOT a “prime” borrower as described above. In the sub-prime market, the lenders set their own qualifying criteria. Many lenders will allow a low score of 580 and still provide 100% financing up to $750,000.00 purchase price! (June 2005)

A sub-prime lender may not require proof of income; this loan product is called stated income. Not available for W-2 employees.

A sub-prime lender will allow DTI ratios of up to 54.49% of GROSS income, verses NET income.

As usual, the higher the risk, the higher the interest rate.

Still attainable, 100% purchase up to $1.5 million purchase price, stated income!

Seems unbelievable, although it is true!

Loan programs fluctuate, and interest rates change

Typically a lender or lending institution will borrow money from the federal government at what is known as the “PRIME” rate. The lender will add a margin, usually 2.5% to 5% or more, (depending on the borrowers qualifying ability) and then lend the money to a borrower. There will also be charges called points. Points refer to a percentage of the loan amount. 1 point of 1.5 million is $15,000.00 The difference between wholesale rates and retail rates is approximately 2 points. $30,000.00 for a $1.5 million loan. Now that is a nice paycheck. Even with a paycheck like that, the brokers that only broker loans in the industry, will want 3 or 4 points! The broker that charges that amount will say, “If the borrower thinks they are getting a good deal, then it is a good deal”. Personally I think there is a point the charges become excessive, the client would have been charged less if they have come to me or my company!

If a borrower walks into there local bank depository, the bank will also borrow money from the federal government, add their margin, and loan it to borrowers. Banks are also allowed to loan up to 94% of every dollar that is deposited into accounts with that bank. If a borrower has a checking account with an average balance of $2,000.00 every month, that bank has loaned $1,880.00 of the depositors $2,000.00 at a rate equal or greater then the “prime” borrower will pay. How much interest did you collect on this deposit? Chances are you received less then ½ of 1%.

That is another way a bank or lending institution makes a profit.

Profits are a good thing! If no profits are made, that business will no longer exist. Unconscionable profits from fraud or deceit are usury or criminal.

Your deposits into a bank are insured up to $100,000.00 per account? If you read the actual insurance, it is our tax paying dollars that insure only principle deposits. If a bank fails, like Lincoln Savings & Loan in 1989 (and all other S&L’s at that time), your deposit (principle only) into an account will be paid back to you in monthly installments, WITHOUT interest! So much for the insured accounts, accounts insured by F.D.I.C. only now, no more F.S.L.I.C.

This description is only the very minimal understanding a buyer, seller or borrower should have.

It is only the ‘tip of the iceberg’ of what is available to know in this industry.

There are investment properties, residential, commercial, industrial and raw land.

There are development opportunities, income opportunities and much more!

There is a secondary market where most of the loans are bought and sold. There are servicing contractors, mortgage insurance companies, and government insured loans. There are private money loans available; including what is called “Hard Money”. Each state has its own rules on lending, and how money is secured by real estate.

The hopes of the author of this writing are to increase the understanding of the reader to the real estate industry and the lending industry associated with real estate. The author is a licensed California Real Estate Broker and practices real estate sales, listings and arranges financing in the Southern California area.

For an interview with a professional, please call 949-488-7653 and I will be happy to answer all of your questions.